| Visual image |

|---|

| Metapattern. One level flat hierarchy. No computations. |

|

| Variation of hierarchy. Multi-level hierarchy. No computations. |

|

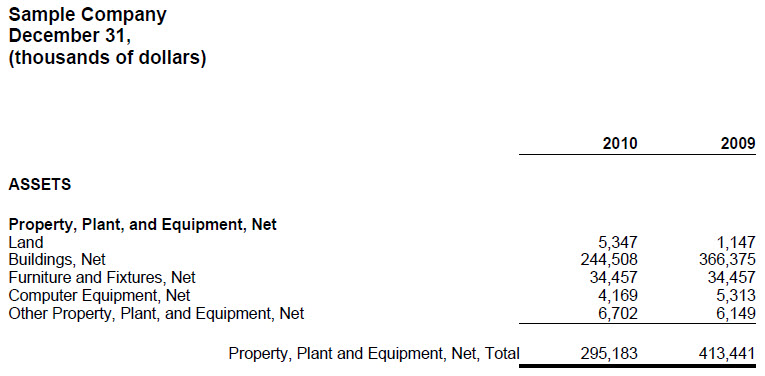

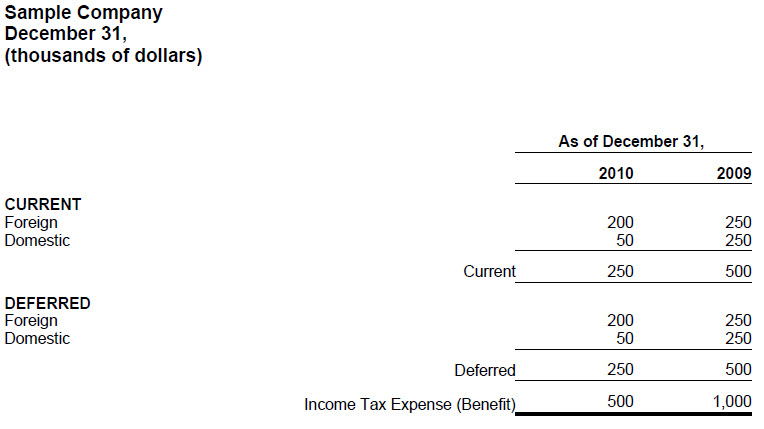

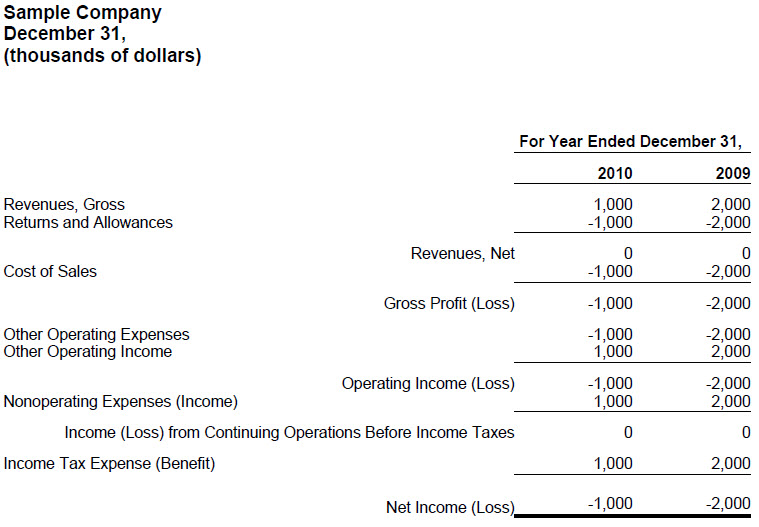

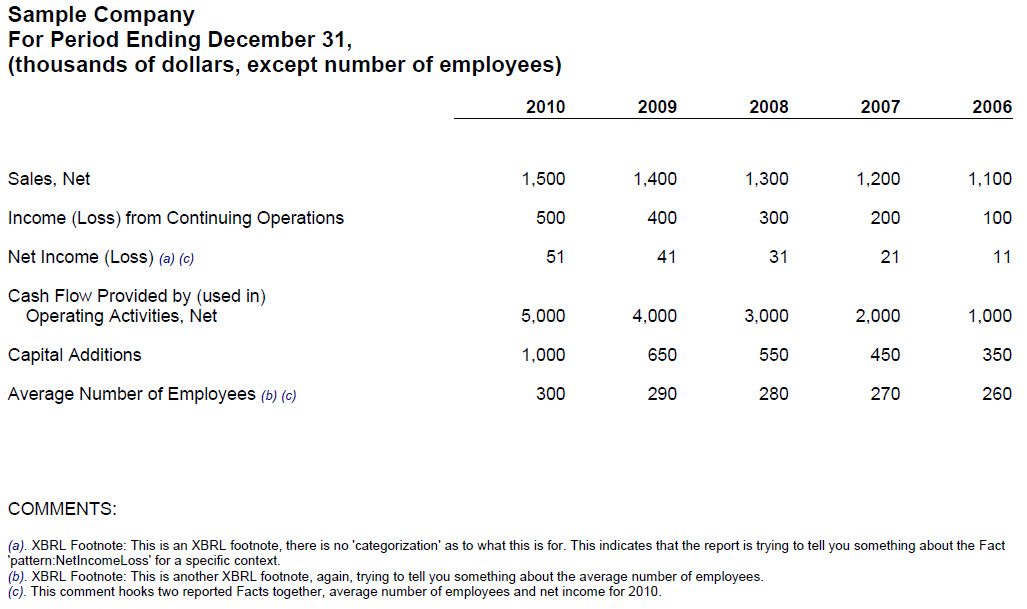

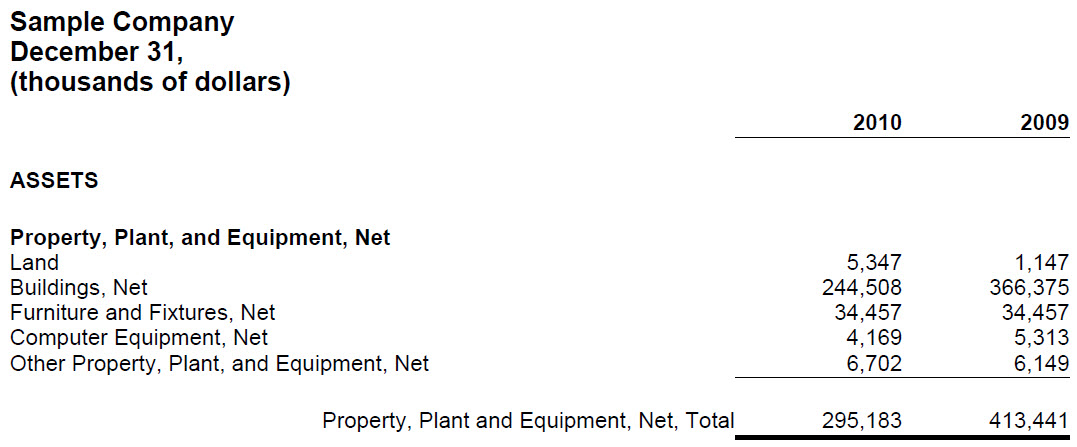

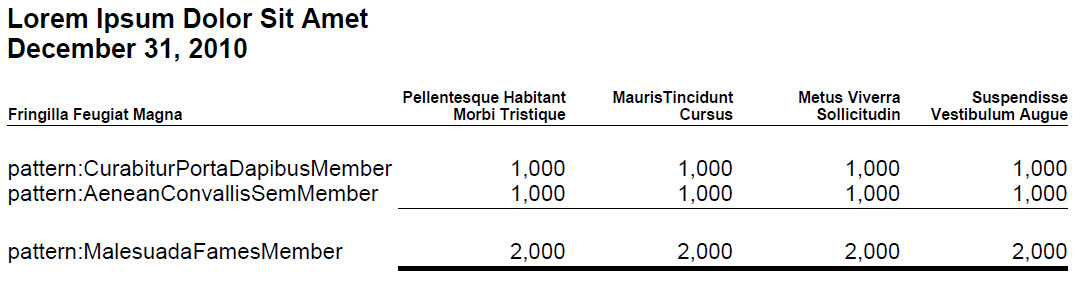

| Metapattern. Simple hierarchy of numeric facts with a roll up type of computation. Computation where A + B + n = Total. |

|

| Variation of roll up. Nesting one roll up inside another roll up. |

|

| Variation of roll up. Multi-level nested roll up. Multiple levels of nested roll ups. |

|

| Variation of roll up. One total rolled up in more than one way forcing roll ups to be expressed within separate networks. |

|

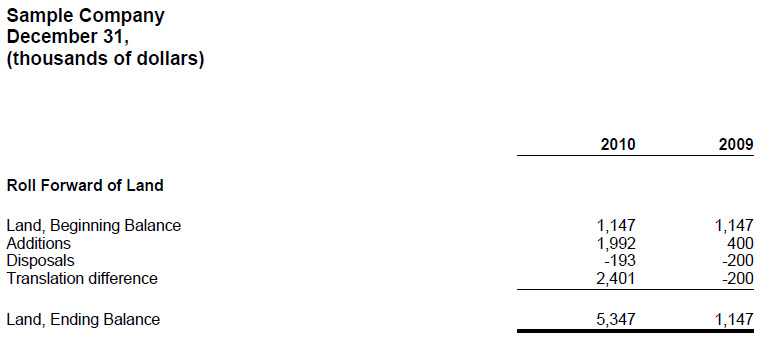

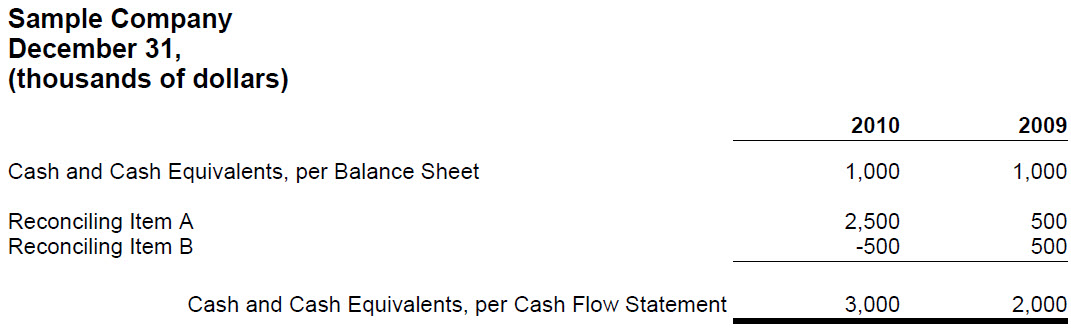

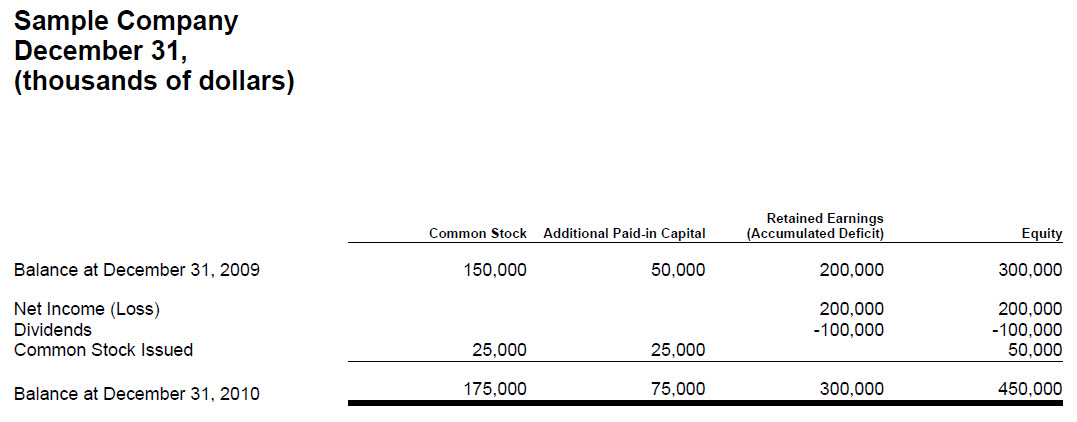

| Metapattern. Simple roll forward of one balance. Also known as movement analysis. Reconciles the changes between two balances, beginning balance + changes = ending balance. |

|

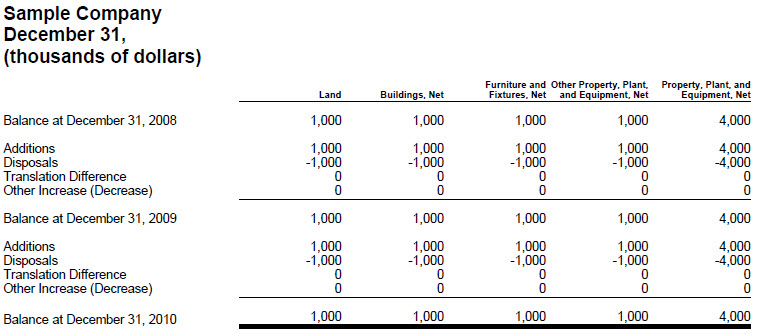

| Variation of roll forward. Roll forward of multiple balances which roll up. |

|

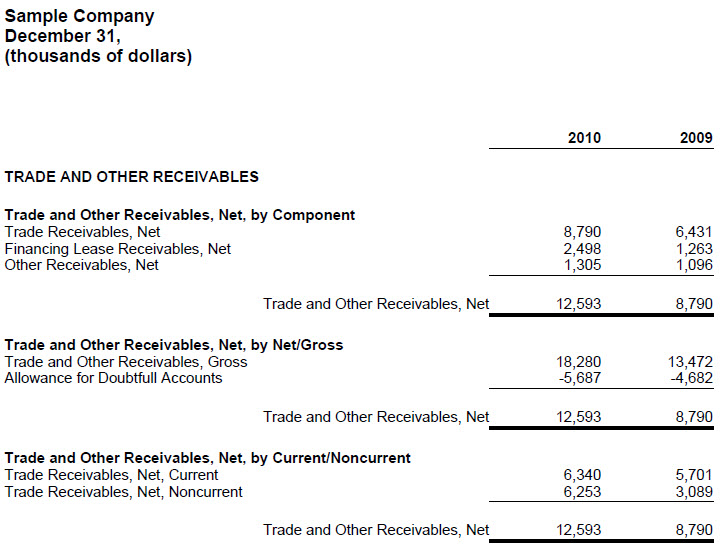

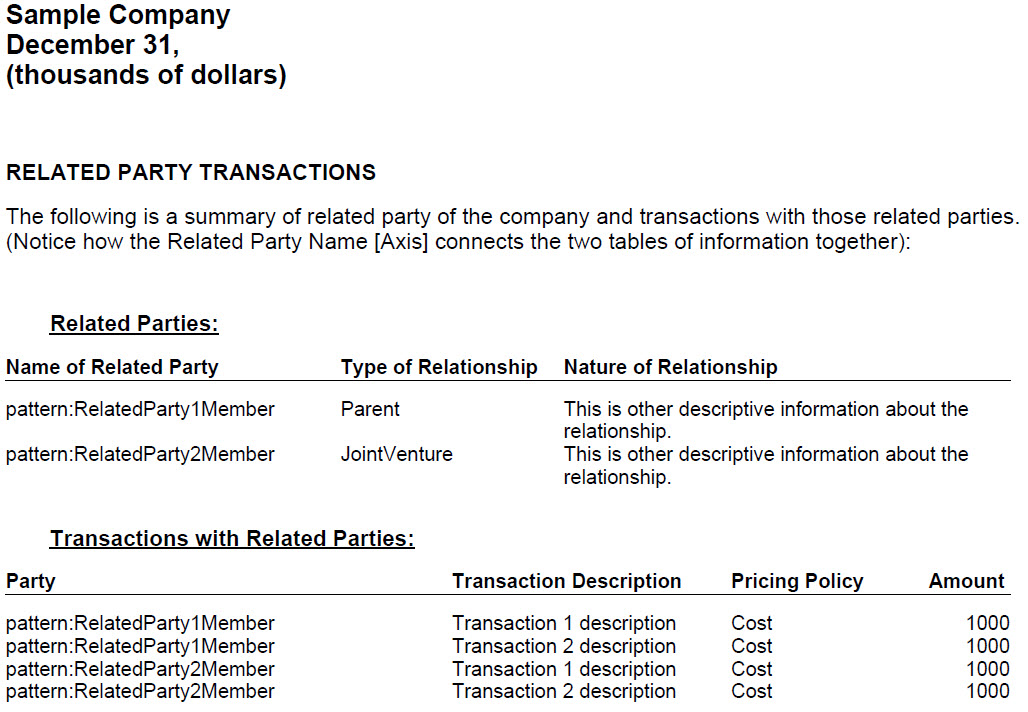

| Metapattern. Set of facts which go together to form a compound fact. Facts are held together by an axis. |

|

| Variation of compound fact. Similar to simple compound fact, points out that fact can repeat. |

|

| Variation of compound fact. Simple compound fact which has more than one period disclosed within the compound fact. |

|

| Variation of compound fact. Roll forward within a compound fact. |

|

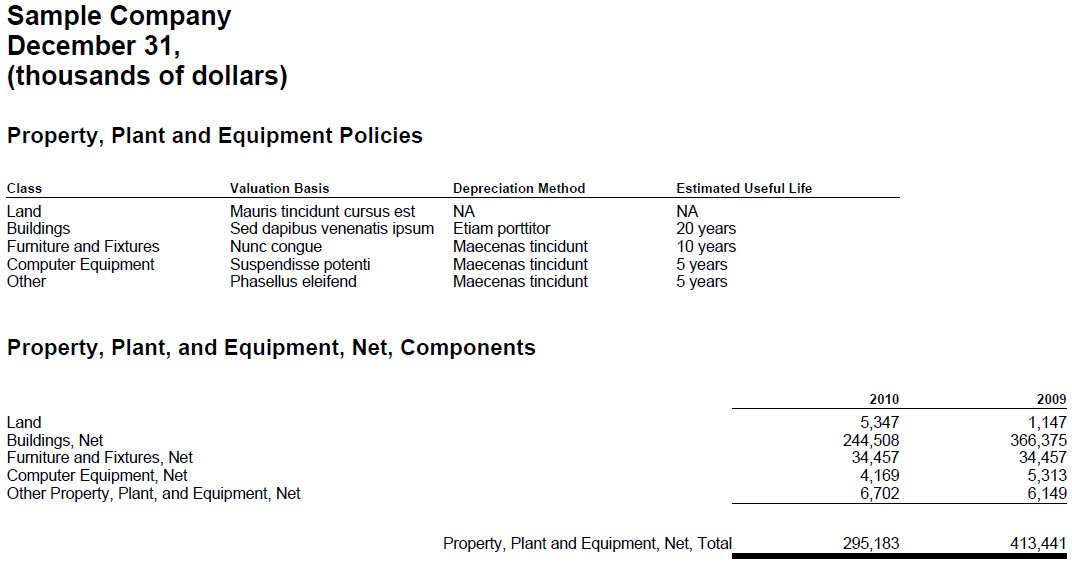

| Variation of compound fact. Compound fact nested within another compound fact. (Good example of different ways to represent characteristics) |

|

| Variation of roll up. Reconciliation of a balance with another balance. (Note that this is not a roll forward.) |

|

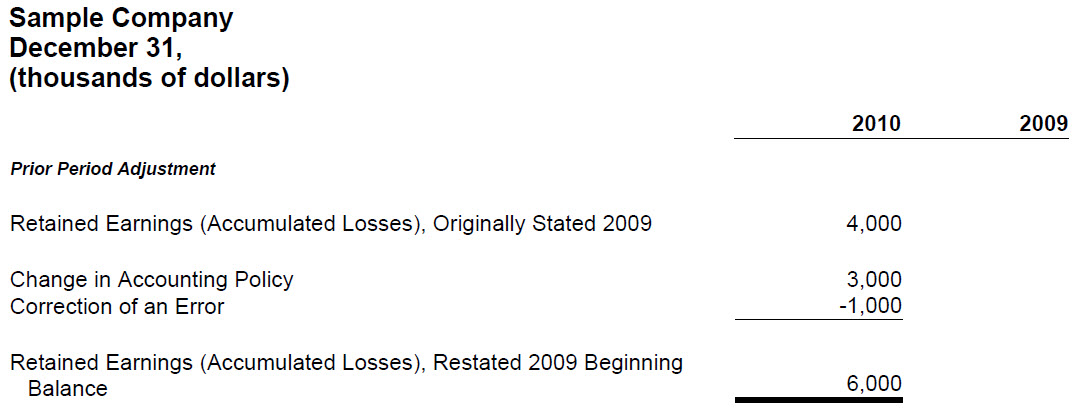

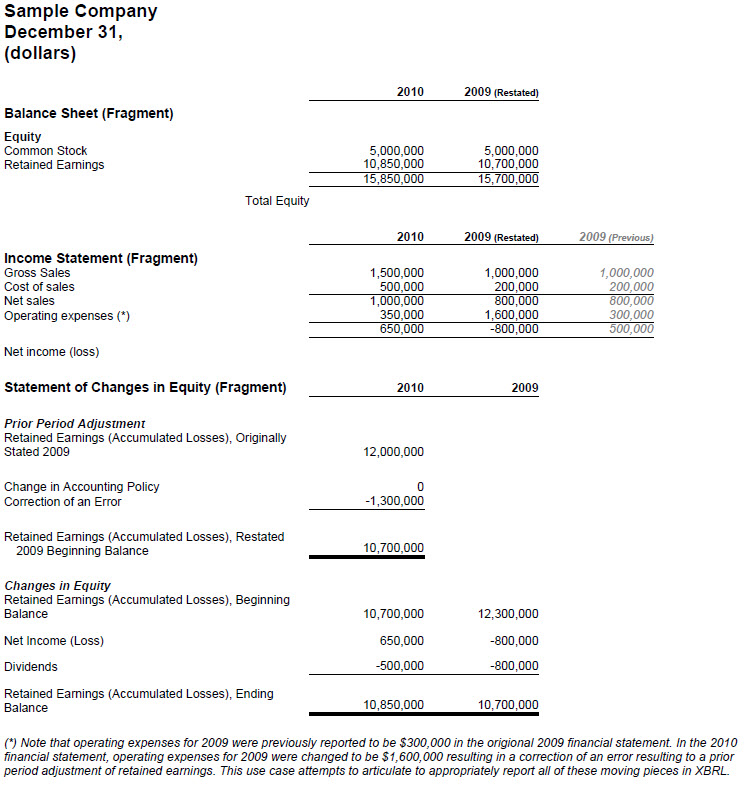

| Reconciles an originally stated balance to a restated balance, the adjustment being the total change, between two different report dates such as a prior period adjustment. |

|

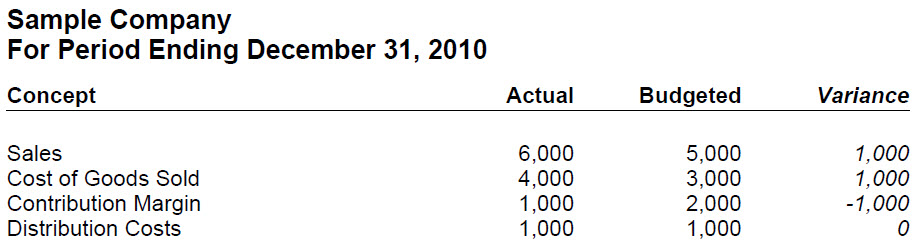

| Reconciles some reporting scenario with another reporting scenario, the variance between reporting scenarios being the variance or changes such as the variance between actual and budget. |

|

| Metapattern. A complex computation information model can be thought of as a hierarchy plus a set of commutations between different concepts within that hierarchy which are challenging to model as the parent/child relations. |

|

| Metapattern. Modelling of what could be modelled as some other information model as one fact. By definition a text block is one fact. |

|

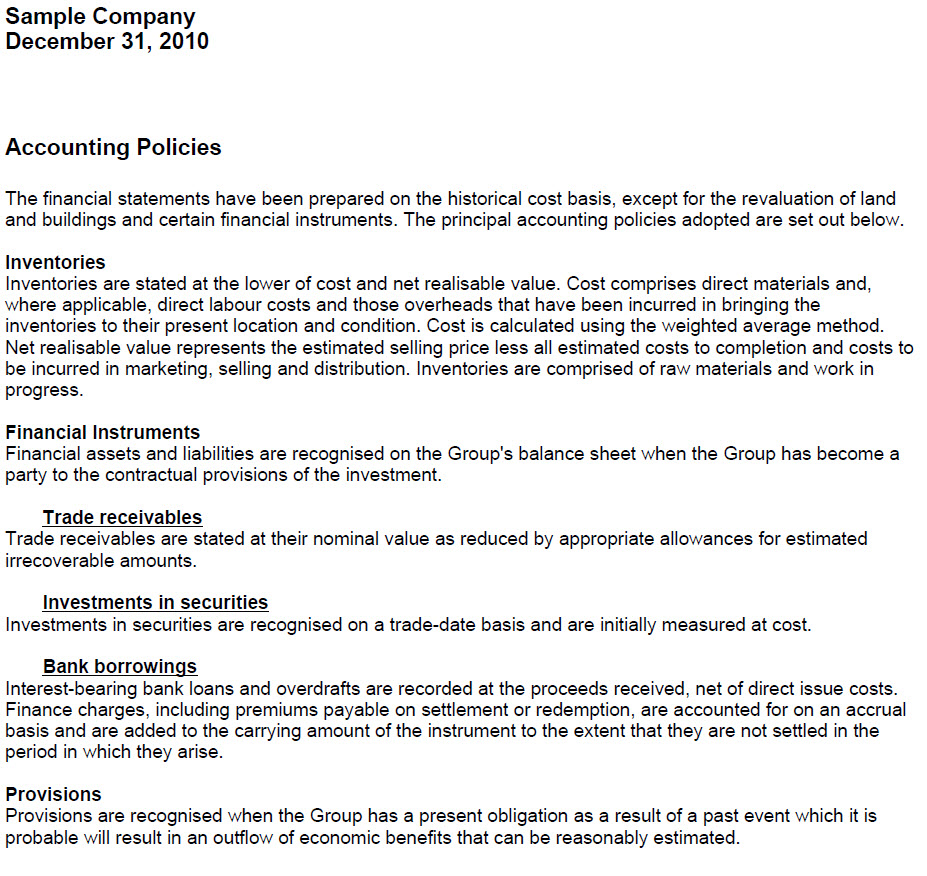

| Information which contains multiple paragraphs, schedules, lists etc. which should appear in a particular order or sequence to be meaningful. |

|

| Variation of text block. Same as prose or text block. Points out how escaped XHTML can be used to report a fact or set of facts. |

|

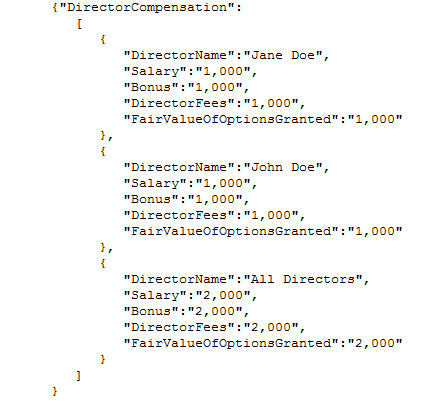

| Variation of text block. Same information contained in the simple compound fact expressed using the JSON syntax. |

|

| Example of a parenthetical explanation. A comment or footnote which expands on or provided additional information for some reported fact. |

|

| Shows how concepts can be related to other concepts and points out the differences between modelling something as a concept and as the member of an axis. |

|

| Shows how concepts related to other concepts can be expressed making the use of an [Axis]. |

|

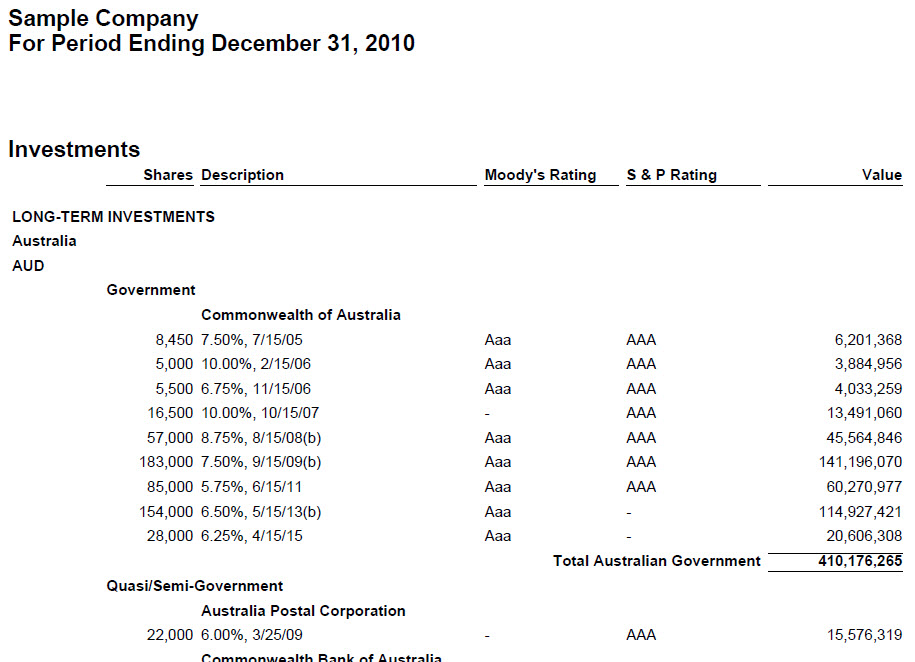

| A grid information model is a pseudo metapattern which uses the presentation characteristics of the columns and rows of a table to model information. (Not recommended) |

|

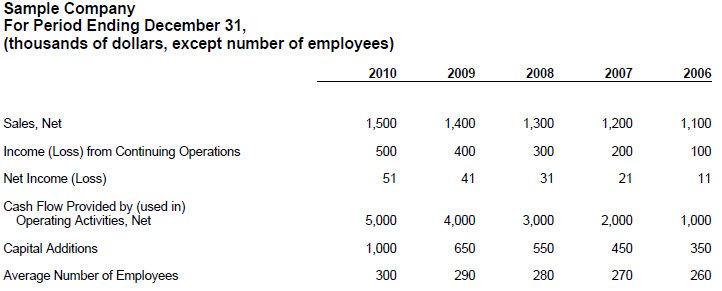

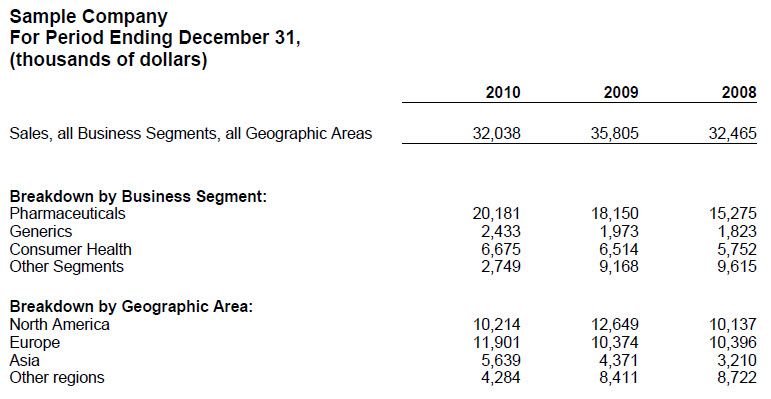

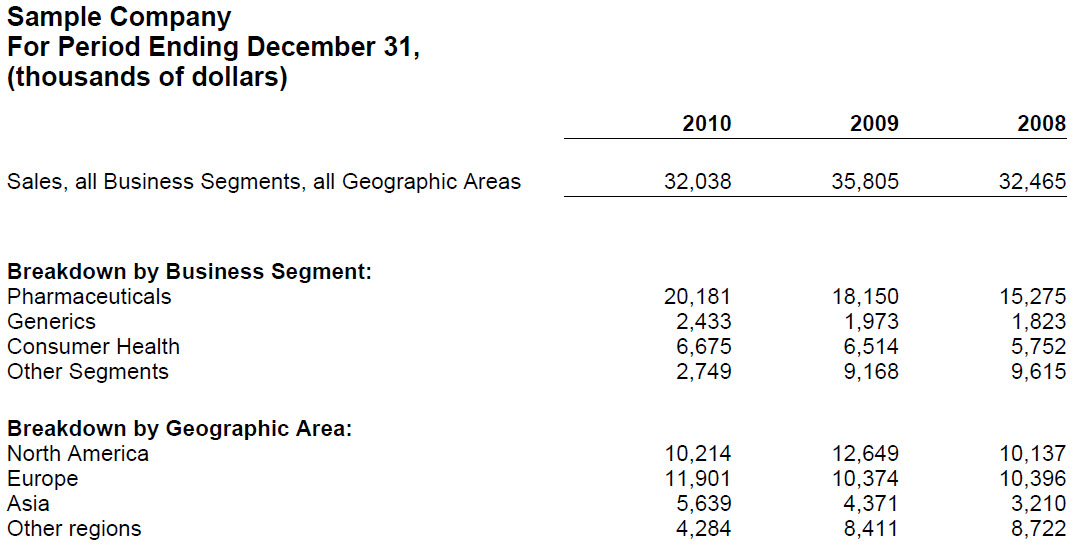

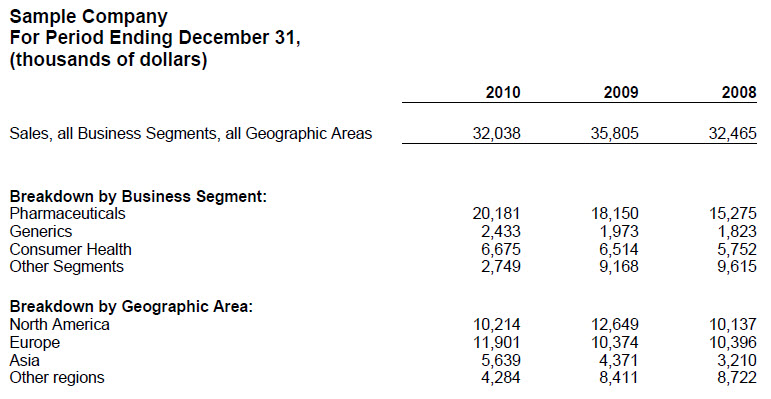

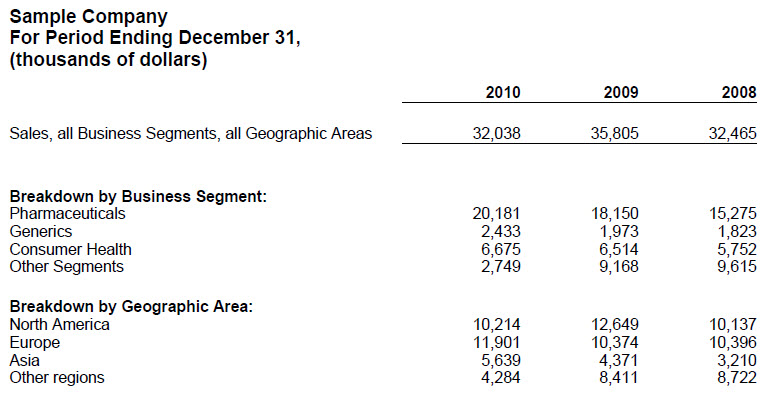

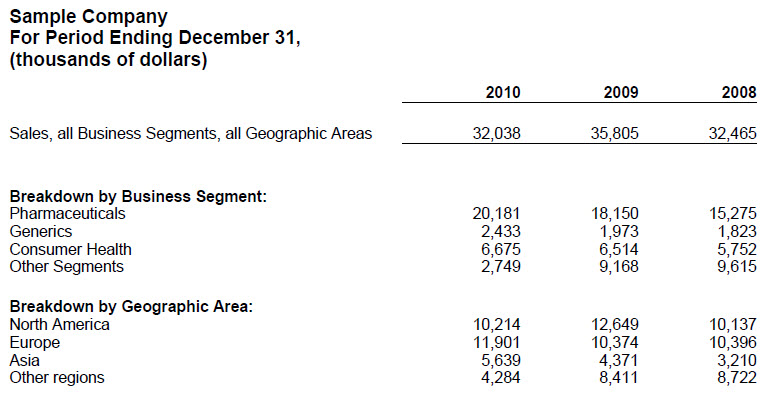

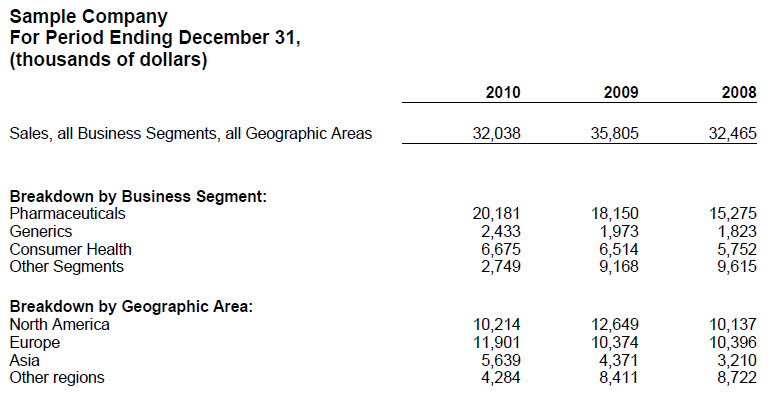

| A set of facts comprised of a single concept which is characterized by one or more axis. Information set is similar to a pivot table. Test Case 1: Explicit hypercube/[Table] exists for Sales Analysis, Summary; Legal Entity [Axis], Business Segment [Axis], Geographic Area [Axis] Explicitly provided |

|

| Variation of compound fact. Table which contains multiple axis which are used to provide information for a complex information set. |

|

| Shows the notion of flow or ordering/sequencing of different tables within a business report and how the ordering or sequencing is important and can be achieved. |

|

| Financial reporting use case of a restatement of income resulting from prior period error or change in accounting policy. |

|

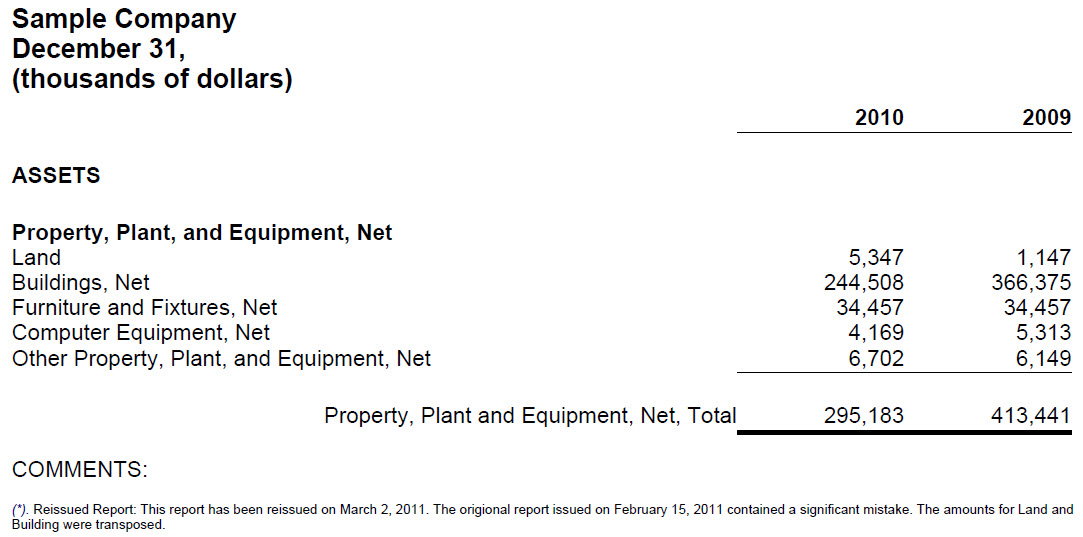

| Financial reporting use case of the reissuance of a report which has already been issued. |

|

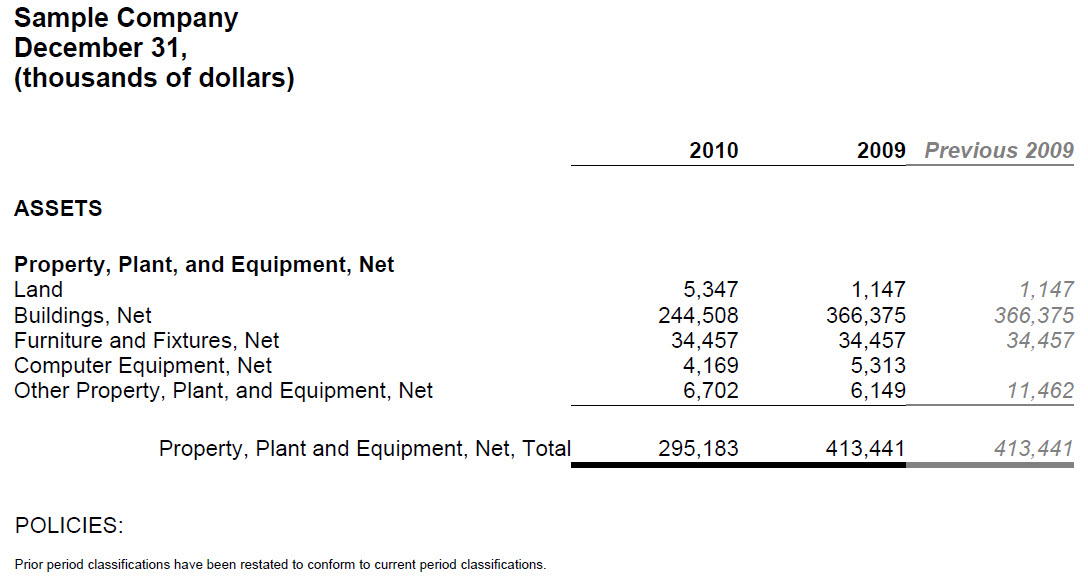

| Financial reporting use case of the reclassification of prior period line items of a report to conform to current period classifications. |

|

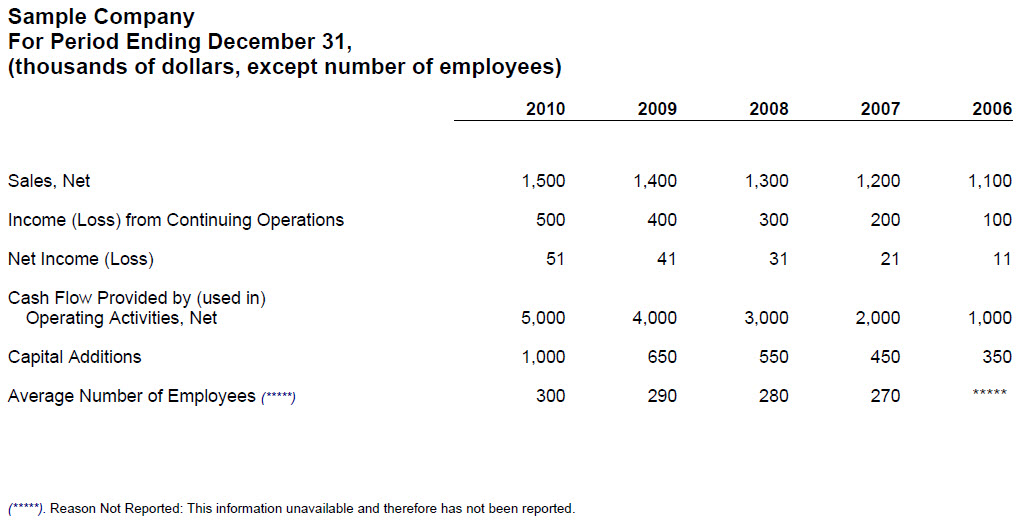

| A specific type of comment or footnote which explains why a fact has not been reported. Points out that footnotes can be differentiated using roles. |

|

| Test Case 2: Explicit hypercube/[Table] exists for Sales Analysis, Summary; Legal Entity [Axis], Business Segment [Axis], Geographic Area [Axis] Explicitly provided |

|

| Test Case 3: Explicit hypercube/[Table] exists for Sales Analysis, Summary; Legal Entity [Axis] Explicitly provided |

|

| Test Case 4: Explicit hypercube/[Table], but no dimensions /[Axes] are explicitly provided |

|

| Test Case 5: No explicit hypercube/[Table] exists for Sales Analysis, Summary |

|

| Shows that there is no difference between expressing financial and non-financial information. |

|

This work is licensed under a Creative Commons License.