1. Introduction

This document specifies the elements of a financial statement, the interrelationships between those elements, and the parts of a financial statement.

ISSUE: This documentation is a work in progress.

1.1 Elements

The following provides formal definitions of the high-level elements of a financial statement. These elements are formally defined by the Australian Accounting Standards Board (AASB) within the AASB 1060 Conceptual Framework. [AASB1060-CONCEPTUAL-FRAMEWORK].

DEBIT

as of point in time

CREDIT

as of point in time

CREDIT

as of point in time

CREDIT

for period of time

DEBIT

for period of time

1.2 Interrelationships

The following provides information about the formal interrelationships between the elements of a financial statement that are either formally defined by the Australian Accounting Standards Board (AASB) within the AASB 1060 Standards or are implied by common practice. [AASB1060-STANDARDS].

1.3 Statements

The following provides information about the formal statements within a set of financial statement that are either formally defined by the Australian Accounting Standards Board (AASB) within SFAC 8 - Elements of Financial Statements [AASB1060-STANDARDS] or are implied and understood common practice.

1.4 Examples

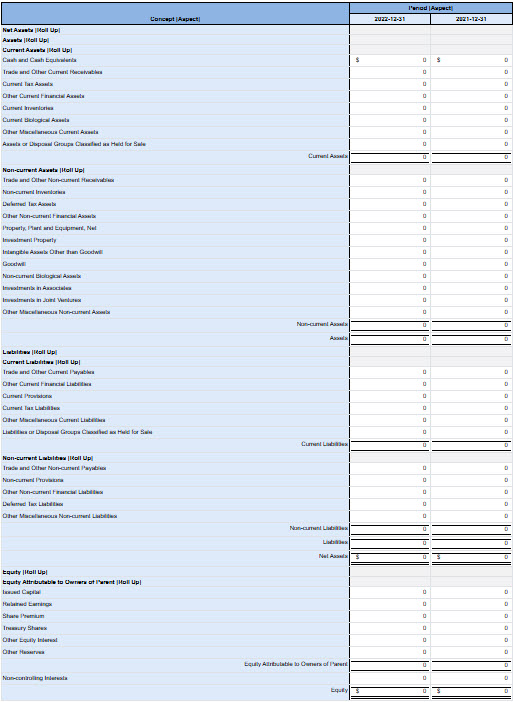

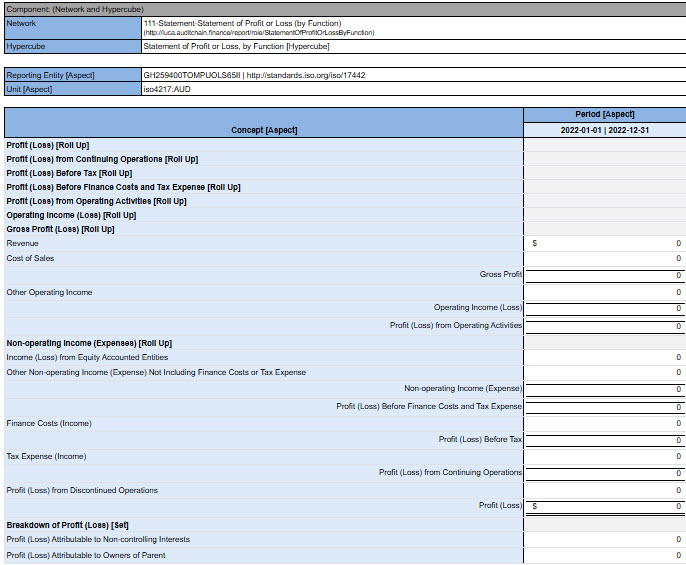

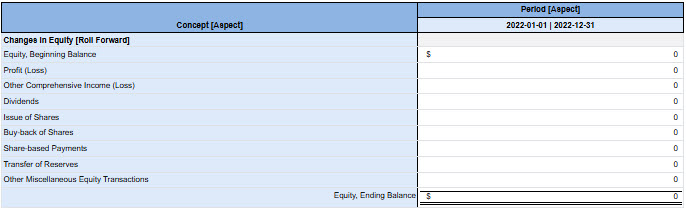

The following are examples of a set of financial statements using the elements of financial statements which conform to the interrelationships of the elements:

1.6 Types

The following graphic shows types and subtypes (a.k.a. general-special assocations, wider-narrower associations) of the elements of financial statements:

1.7 References

The following is a summary of normative and informative references helpful in understanding this information:

1.7.1 Normative references

- [AASB1060-CONCEPTUAL-FRAMEWORK]

- AASB 1060 Conceptual Framework. Australian Accounting Standards Board (AASB). General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities. June 2021. URL: https://xbrlsite.azurewebsites.net/2021/reporting-scheme/aasb1060/standards/Conceptual_Framework_05-19.pdf

- [AASB1060-STANDARDS]

- General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities. Australian Accounting Standards Board (AASB). June 2021. URL: https://xbrlsite.azurewebsites.net/2021/reporting-scheme/aasb1060/standards/AASB1060_Amendments_03-20.pdf

- [AASB1060-MODEL]

- AASB 1060 Financial Reporting Scheme Working Prototype. Australian Accounting Standards Board (AASB). General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities. June 2021. URL: https://xbrlsite.azurewebsites.net/2021/reporting-scheme/aasb1060/base-taxonomy/aasb1060_ModelStructure2.html

- [AASB1060-REFERENCE]

- REFFERENCE IMPLEMENTATION of AASB 1060 Report. Charles Hoffman, CPA. 2024. URL: https://auditchain.infura-ipfs.io/ipfs/QmedrzwbaBqrwyr6mNMMrF9VyQppfGuT1FgN3wY4KJaD4x

1.7.2 Informative references

- [AASB1060-EXAMPLE]

- Two AASB 1060 Reports to Fiddle With. Charles Hoffman, CPA. 03 June 2024. URL: https://digitalfinancialreporting.blogspot.com/2024/01/two-aasb-1060-reports-to-fiddle-with.html