1. Introduction

This resource specifies the common practice definition of the accounting equation. The purpose of this resourcse is to explicit, clear, and complete.

The accounting equation, also called the fundamental accounting equation and the balance sheet equation, is the foundation for the double-entry bookkeeping system and the cornerstone of accounting science.

1.1 Elements

The following provides the common practice, informal defintion of the accounting equation. [ACCOUNTING-EQUATION].

DEBIT

as of point in time

CREDIT

as of point in time

CREDIT

as of point in time

1.2 Interrelationships

The following provides information about the formal interrelationships between the elements of the accounting equation [ACCOUNTING-EQUATION] or are implied and understood common practice.

1.3 Statements

The following resource provides information about the cornerstone of financial concepts, the accounting equation. [ACCOUNTING-EQUATION]. The accounting equation is well understood

1.4 Examples

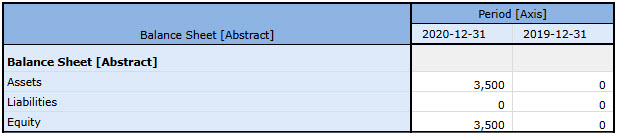

The following is an example of a balance sheet which contains the elements of the accounting equation which conform to the interrelationships of the elements:

1.6 Types

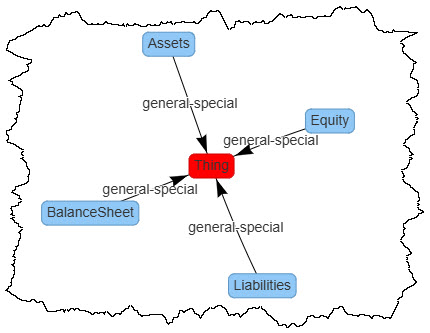

The following graphic shows types and subtypes (a.k.a. general-special assocations, wider-narrower associations) of the elements of financial statements:

1.7 References

The following is a summary of normative and informative references helpful in understanding this information:

1.7.1 Normative references

- [ACCOUNTING-EQUATION]

- Accounting Equation. Financial Accounting Standards Board (FASB). 2004. URL: https://en.wikipedia.org/wiki/Accounting_equation

- [AE-PROOF]

- PROOF. AE PROOF. 2024. URL: https://auditchain.infura-ipfs.io/ipfs/QmPeD6DrM8xsgwiSnwo6JR1njJmurDgBkQQf1kLAooJRwh/

1.7.2 Informative references

- [AE-MODEL]

- Accounting Equation MODEL. Charles Hoffman, CPA. 03 June 2024. URL: http://xbrlsite.com/seattlemethod/platinum/ae/ae_ModelStructure.html

- [REFERENCE-IMPLEMENTATION]

- Accounting Equation Reference Implementation. Charles Hoffman, CPA. 03 June 2024. URL: http://xbrlsite.com/seattlemethod/platinum/ae/index.html

- [DOCUMENTATION]

- Accounting Equation Documentation. Charles Hoffman, CPA. 03 June 2024. URL: http://xbrlsite.com/seattlemethod/platinum/ae/AE-Impediments.pdf