This resource introduces the notion of a financial reporting scheme providing what amounts to the first example that looks like a real, although basic, financial

reporting scheme. This financial reporting scheme is limited however, it does not make use of dimensions.

1. Introduction

This document specifies a financial reporting scheme referred to as MINI Financial Reporting Scheme. This financial reporting scheme is a training tool.

1.1 Elements

The following provides formal definitions of the high-level elements of a financial statement. These elements are formally defined by the MINI Accounting Standards Board (MASB)

[MINI].

Assets

Assets are probable future sacrifices of econmic benefits arising from present obligations of a particular entity to transfer assets or provide services to other entities in the future as a result

of past transactions.

DEBIT

as of point in time

Liabilities

Liabilities are probable future sacrifices of economic benefits arising from present obligations of a particular entity to transfer assets or provide services to other entities in the future as a result

of past transactions.

CREDIT

as of point in time

Equity

Equity or net assets is the residual interest in the assets of an entity that remains after deducting its liabilities. In a business enterprise, the equity is the ownership interest. In a not-for-profit

organization, which has no ownership interest in the same sense as a business enterprise, net assets is divided into three classes based on the presence or absense of donor-imposed restrictions: permanentaly restricted,

temporarily restricted, and unrestricted net assets.

CREDIT

as of point in time

Comprehensive Income

Comprehensive income is the change in equity of a business enterprise during a period from transactions and other events and circumstances from nonowner sources. It includes all changes in equity during a period except those

resulting from investments by owners and distributions to owners.

CREDIT

for period of time

Investments by Owners

Investments by owners are increases in equity of a particular business enterprise resunting from transfers to it from other entities of something valuable to obtain or increase ownership interests (or equity) in it.

Assets are most commonly recieved as investments by owners, but that which is received may also include services or satisfaction or conversion of liabilities of the enterprise.

DEBIT

for period of time

Distributions to Owners

Distributions to owners are decreases in equity of a particular business enterprise resulting from transferring assets, rendering services, or incurring liabilities by the enterprise to owners. Distributions to owners

decrease ownership interest (or equity) in an enterprise.

CREDIT

for period of time

Revenues

Revenues are inflows or other enhancements of assets of an entity or settlements of its liabilities (or a combination of both) from delivering or producing goods, rendering services, or other activities

that constitute the entity's ongoing major or centeral operations.

CREDIT

for period of time

Expenses

Expenses are outflows or other using up of assets or incurrences of liabilities (or a combination of both) from delivering of producing goods, rendering of services, or carrying out of activities

that constitute the entity's ongoing major or central operations.

DEBIT

for period of time

Gains

Gains are increases in equity (net assets) from peripheral or incidental transactions of an entity and from all other transactions and other events and circumstances affecting the entity except

those that result from revenues or investments by owners.

CREDIT

for period of time

Losses

Losses are decreases in equity (net assets) from peripheral or incidental transactions of an entity and from all other transactions and other events and circumstances affecting the entity except those that result

from expenses or distributions of services.

DEBIT

for period of time

1.2 Interrelationships

The following provides information about the formal interrelationships between the elements of a financial statement that are either formally defined by the MINI Accounting Standards Board (MASB)

[MINI] or are implied and understood common practice.

Assets = Liabilities + Equity

The accounting equation; the sum of Assets is equal to the sum of Liabilities plus the sum of Equity. The accounting equation is well understood common practice. For additional information see:

Wikipedia, Accounting Equation

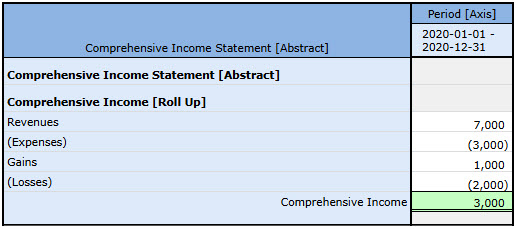

Comprehensive income = Revenues - Expenses + Gains - Losses

Comprehensive income is comprised of the sum of Revenues less the sum of Expenses plus the sum of Gains minus the sum of Losses.

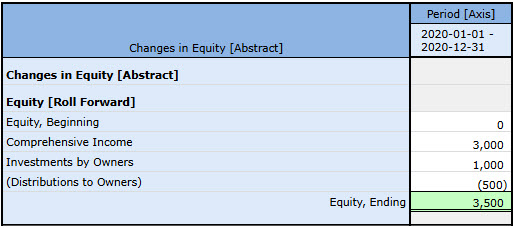

Equity(T1) = Equity(T0) + Comprehensive income(P1) + Investments by owners(P1) - Distributions to owners(P1)

The ending balance of Equity (T1) is equal to the beginning balance of equity (T0) plus Comprehensive income for the period (P1) plus Investments by owners during the period (P1) less Distributions to owners during the period (P1).

The ending balance of Equity (T1) is equal to the beginning balance of Equity (T0) plus the components of Comprehensive Income for Comprehensive income for the period (P1) (Revenues, Expenses, Gains, Losses)

plus Investments by Owners during the period (P1) less Distributions to Owners during the period (P1) plus Liabilities(T1) less Assets(T1).

1.3 Statements

The following provides information about the formal statements within a set of financial statement that are either formally defined by the MINI Accounting Standards Board (FASB)

[MINI] or are implied and understood common practice.

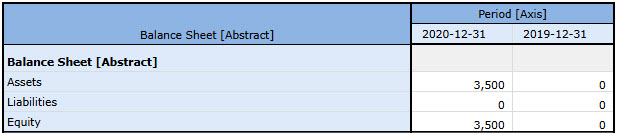

Statement of Financial Position

A Statement of Financial Position (a.k.a. Balance Sheet) is used to report the elements Assets, Liabilities and Equity.

Statement of Financial Condition

A Statement of Financial Condition (a.k.a. Income Statement, Statement of Operations) is used to report Revenues, Expenses, Gains, Losses, and Comprehensive Income.

Statement of Changes in Equity

A Statement of Changes in Equity is used to report Equity, Comprhensive Income, Investments by Owners, Distributions to Owners.

1.4 Examples

The following are examples of a set of financial statements using the elements of financial statements which conform to the interrelationships of the elements:

Statement of Financial Position

Statement of Financial Condition

Statement of Changes in Equity

1.5 Transactions

The following graphic shows the relationships between transactions, statements, and elements of financial statements: (Business events)

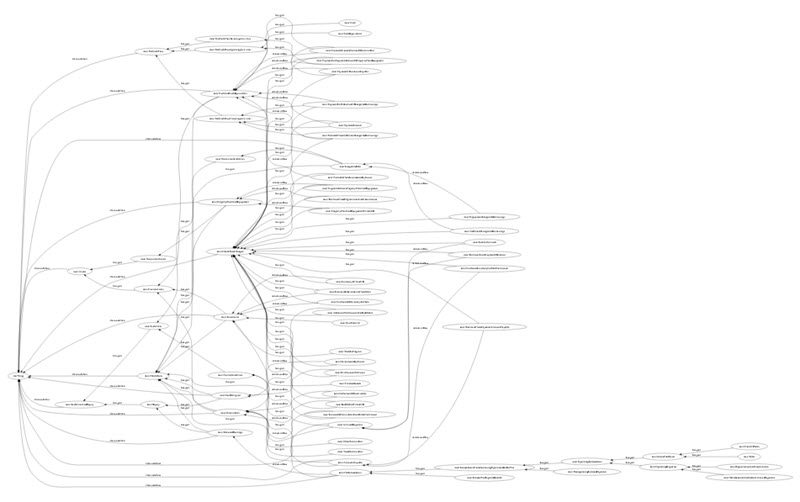

1.6 Types

The following graphic shows types and subtypes (a.k.a. general-special assocations, wider-narrower associations) of the elements of financial statements:

1.7 References

The following is a summary of normative and informative references helpful in understanding this information: