1. Introduction

This document specifies the elements of a financial statement, the interrelationships between those elements, and the parts of a financial statement for a bank. Note that the OCC does not lay this information out as sustinctly or as completely. The purpose of this resourcse is to clear and complete.

"Particular economic things and events, such as cash on hand or selling merchandise, that may meet the definitions of elements are not elements as the term is used in this Statement. Rather, they are called items or other descriptive names. This Statement focuses on the broad classes and their characteristics instead of defining particular assets, liabilities, or other items."

***** NOTE ***** This version of reporting scheme documentation is similar to W3C recommendations and seems desirable because you can link directly to an identifier in this document. Linking directly to point in a PDF document is possible, but this seems superior.

1.1 Elements

The following provides formal definitions of the high-level elements of a financial statement. These elements are formally defined by the Office of Comptroller of Currency (OCC) within available documentation [OCC].

DEBIT

as of point in time

CREDIT

as of point in time

1.2 Interrelationships

The following provides information about the formal interrelationships between the elements of a financial statement that are either formally defined by the Office of Comptroller of Currency (OCC) within available documentation [OCC] or are implied and understood common practice.

1.3 Statements

The following provides information about the formal statements within a set of financial statement that are either formally defined by the Office of the Comptroller of Currency (OCC) within OCC rules [OCC] or are implied and understood common practice.

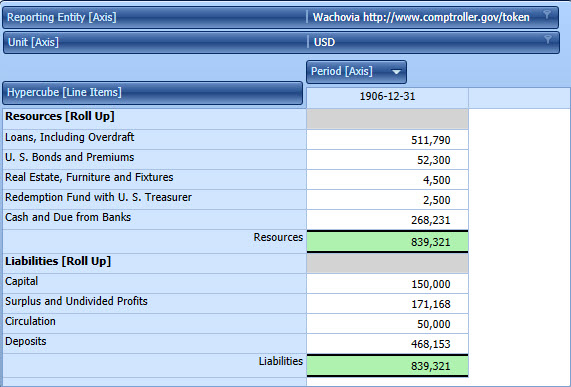

1.4 Examples

The following are examples of a set of financial statements using the elements of financial statements which conform to the interrelationships of the elements:

1.5 Transactions

The following graphic shows the relationships between transactions, statements, and elements of financial statements:

![]()

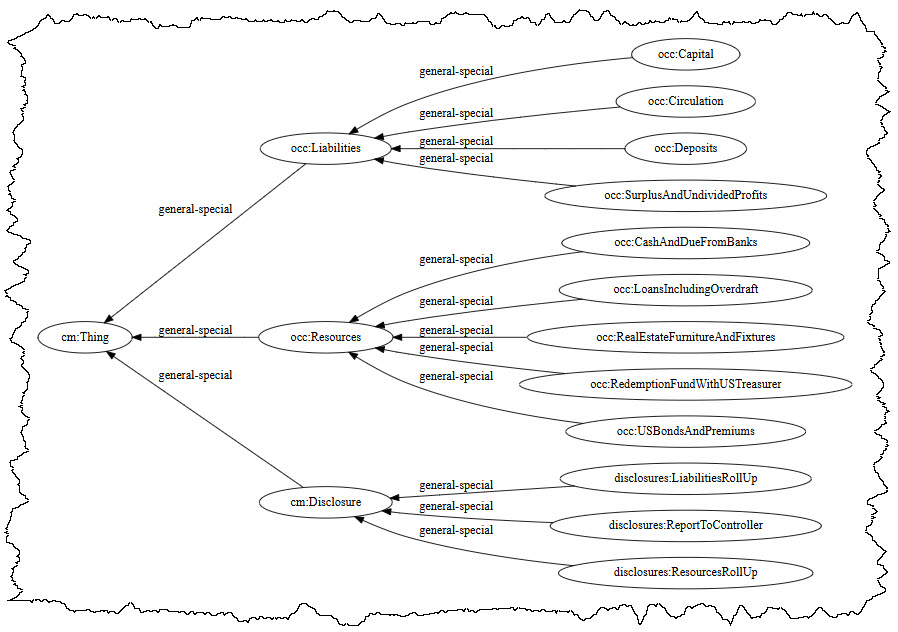

1.6 Types

The following graphic shows types and subtypes (a.k.a. general-special assocations, wider-narrower associations) of the elements of financial statements:

1.7 References

The following is a summary of normative and informative references helpful in understanding this information:

1.7.1 Normative references

- [OCC]

- Report to Comptroller. Office of the Comptroller of Currency (OCC). 2004. URL: https://www.occ.gov/

1.7.2 Informative references

- [OCC-MODEL]

- OCC MODEL. Charles Hoffman, CPA. 03 June 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/occ/base/occ_ModelStructure.html

- [EXAMPLE]

- Example Financial Statement. Charles Hoffman, CPA. 03 June 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/occ/ref/index2.html

- [EXAMPLE2]

- Example Financial Statement from Wikipedia. Charles Hoffman, CPA. 03 June 2024. URL: https://en.wikipedia.org/wiki/Financial_statement#Purpose_of_financial_statements