1. Introduction

This resource is designed to look similar to a financial statement; but is more about understanding the logical patterns that exist within the information contained within a financial report.

This is an excellent teaching tool and software testing resource.

1.1 Elements

The following provides formal definitions of the high-level elements of a financial statement. These elements are informally defined by common practice. [FINANCIAL-STATEMENT]. [TERMS].

DEBIT, as of point in time

CREDIT, as of point in time

CREDIT, as of point in time

CREDIT, for period of time

DEBIT, for period of time

CREDIT, for period of time

CREDIT, for period of time

DEBIT, for period of time

CREDIT, for period of time

DEBIT, for period of time

CREDIT, for period of time

CREDIT, for period of time

DEBIT, for period of time

DEBIT, for period of time

DEBIT, for period of time

DEBIT, for period of time

1.2 Interrelationships

The following provides information about the formal interrelationships between the elements of a financial statement that are informally defined by common practice. [FINANCIAL-STATEMENT] or are implied and understood common practice. [REPORT-MATH-FORMULAS]. [REPORT-MATH-ROLLUPS].

1.3 Statements

The following provides information about the formal statements within a set of financial statement that are informally defined by common practice and not disputed. [FINANCIAL-STATEMENT].

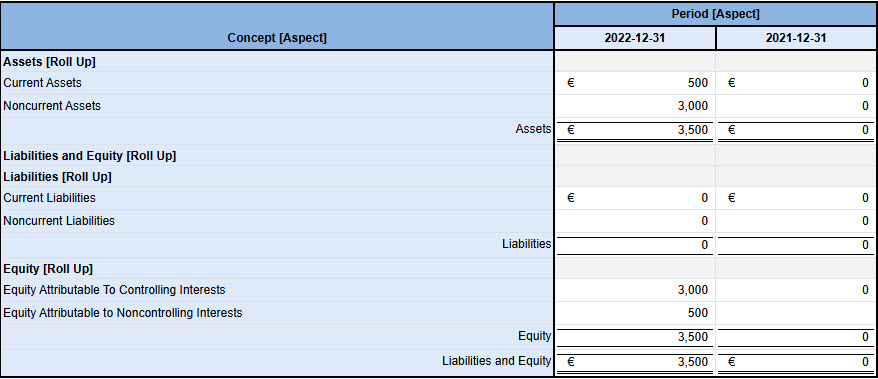

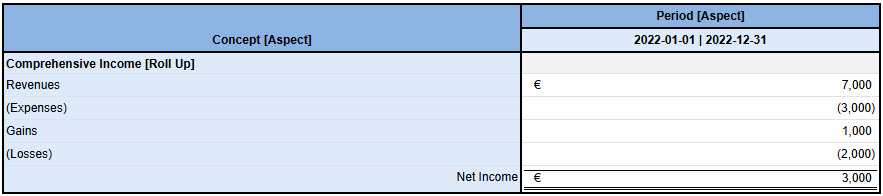

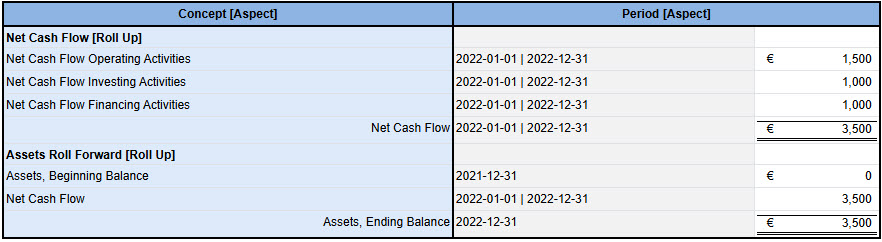

1.4 Examples

The following are examples of a set of financial statements using the elements of financial statements which conform to the interrelationships of the elements:

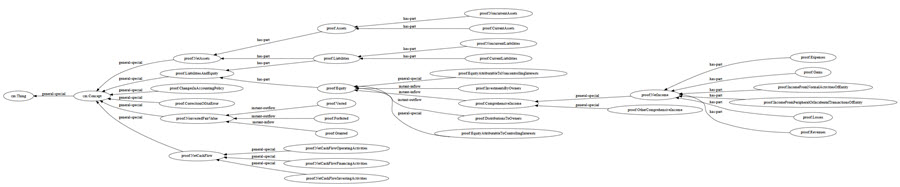

1.6 Types

The following graphic shows types and subtypes (a.k.a. general-special assocations, wider-narrower associations) of the elements of financial statements: [TYPES-BSC-IS01-CF1]

1.7 References

The following is a summary of normative and informative references helpful in understanding this information:

1.7.1 Normative references

- [FINANCIAL-STATEMENT]

- Financial Statement. Wikipedia. Retrieved June 11, 2024. URL: https://en.wikipedia.org/wiki/Financial_statement

- [PROOF-VERIFICATION]

- PROOF Verification Results. June 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/ref/pacioli/index.html

1.7.2 Informative references

- [PROOF-MODEL]

- PROOF. Charles Hoffman, CPA. June 2024. URL: http://xbrlsite.com/seattlemethod/platinum/proof/base-taxonomy/proof_ModelStructure.html

- [PROOF-REFERENCE-IMPLEMENTION]

- Reference Implementation of PROOF. Charles Hoffman, CPA. 03 June 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/ref/index2.html

- [PROOF-DOCUMENTATION]

- PROOF Blog Post. Charles Hoffman, CPA. 03 June 2024. URL: https://digitalfinancialreporting.blogspot.com/2023/12/proof.html

- [SUPER-PROOF]

- PROOF Blog Post. Charles Hoffman, CPA. 03 June 2024. URL: https://digitalfinancialreporting.blogspot.com/2024/05/super-proof.html

1.8 Technical (Appendix)

The following are technical artifacts related to this resource:

1.8.1 Machine readable artifacts

- [ENTRY-POINT]

- Entry point of financial reporting scheme. PROOF. June 11, 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/base-taxonomy/proof-entryPoint.xsd

- [TERMS]

- Terms of financial reporting scheme; also hooked to Labels and References for Terms. PROOF. June 11, 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/base-taxonomy/proof.xsd

- [STRUCTURES]

- Structures of financial reporting scheme. PROOF. June 11, 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/base-taxonomy/proof-roles.xsd

- [DISCLOSURES]

- Disclosures of financial reporting scheme. PROOF. June 11, 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/disclosures-topics/disclosures.xsd

- [DISCLOSURE-MECHANICS]

- Disclosure mechanics rules of financial reporting scheme. PROOF. June 11, 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/disclosure-mechanics/disclosure-mechanics.xsd

- [TOPICS]

- Topics of financial reporting scheme. (Used to organize disclosures.). PROOF. June 11, 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/disclosures-topics/topics.xsd

- [REPORTING-STYLES]

- Reporting Styles of financial reporting scheme.. PROOF. June 11, 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/fac/reporting-styles-cm-ref.xml

- [FAC-BSC-IS01-CF1]

- Fundamental Accounting Concepts (FAC) of BSC-IS01-CF1 reporting style for financial reporting scheme.. PROOF. June 11, 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/fac/reporting-styles/BSC-IS01-CF1_schema.xsd

- [TYPES-BSC-IS01-CF1]

- Types of BSC-IS01-CF1 reporting style for financial reporting scheme.. PROOF. June 11, 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/type-subtype/types-BSC-IS01-CF1-rules-def.xml

- [REPORTING-CHECKLIST-BSC-IS01-CF1]

- Reporting Checklist of BSC-IS01-CF1 reporting style for financial reporting scheme.. PROOF. June 11, 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/reporting-checklist/reporting-checklist-BSC-IS01-CF1-rules-def.xml

- [MODEL-STRUCTURE-RULES]

- Structures of financial reporting scheme. PROOF. June 11, 2024. URL: http://xbrlsite.com/seattlemethod/cm/model-structure-rules-strict-def.xml

- [REPORT-MATH-FORMULAS]

- REPORT Math, XBRL Formulas of report. June 11, 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/ref-BSC-IS01-CF1/report-for.xml

- [REPORT-MATH-ROLLUPS]

- REPORT Math, XBRL Calculations relations of report. June 11, 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/ref-BSC-IS01-CF1/report-cal.xml

- [REPORT-MODEL]

- REPORT Model, XBRL Presentation relations of report. June 11, 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/ref-BSC-IS01-CF1/report-pre.xml

1.8.2 Human readable artifacts

- [HTML]

- Human readable HTML rendering of report. PROOF. June 11, 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/ref-BSC-IS01-CF1/LUCA_REPORT.html

- [REPORTING-SCHEME]

- Human readable HTML rendering of reporting scheme XBRL presentation relations. PROOF. June 11, 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/base-taxonomy/proof_ModelStructure.html

- [WIDER-NARROWER]

- Human readable WIDER-NARROWER relations. PROOF. June 11, 2024. URL: http://www.xbrlsite.com/seattlemethod/platinum/proof/ref-BSC-IS01-CF1/types-humanReadable.jpg